If you’ve been in commercial real estate for any length of time, you already know the drill: raw land is cheap. It’s the entitlements, the utility capacity, the road access, and the patience to survive 18–24 months of permitting and construction that actually make a deal pencil out. Take any one of those pieces away and your pro forma falls apart—no matter how strong the demand looks on paper.

Now run that same playbook on the fastest-growing asset class in the entire built environment—AI data centers—and the math flips in a way that should make every developer and investor sit up straight. In 2026, the binding constraint isn’t land, capital, or even the GPUs everyone talks about. It’s electric power: the ability to procure it, transmit it, and actually get it connected to the grid. Power has officially become the new “location.” And the entire commercial real estate playbook for scarcity, entitlements, infrastructure moats, and adaptive reuse translates almost one-to-one.

The Demand Curve That’s Rewriting the Rules

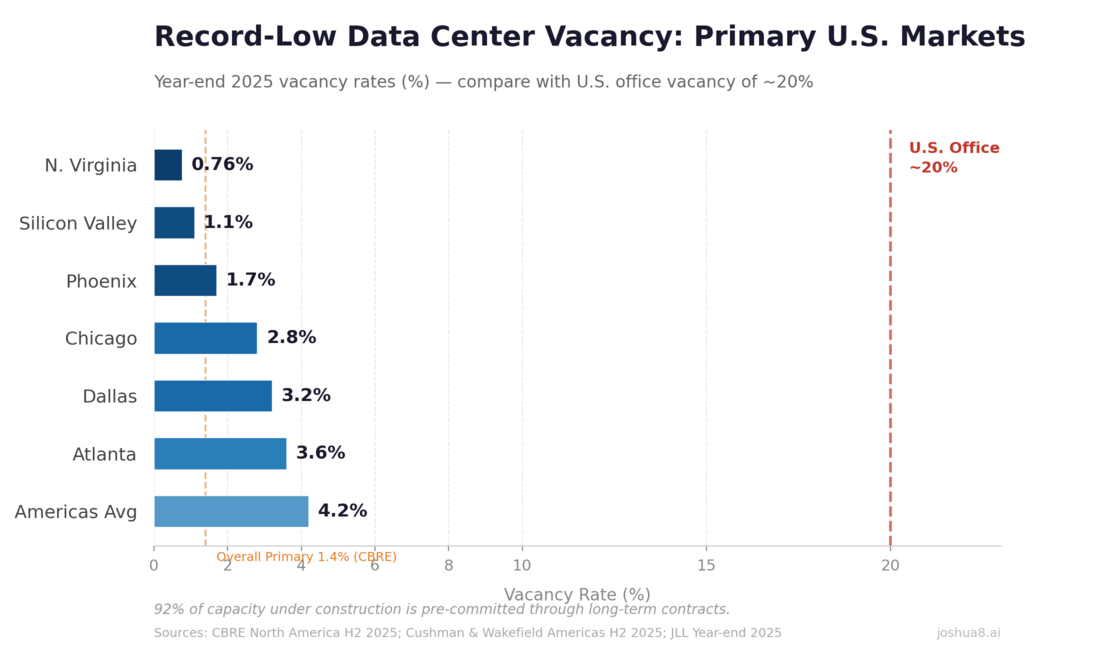

The numbers are no longer theoretical. CBRE’s North America Data Center Trends reports and Cushman & Wakefield’s Americas updates show another record year for leasing, with vacancy rates at historic lows across primary markets—even after massive new supply deliveries. JLL projects nearly 100 GW of new global capacity added between 2026 and 2030 (doubling the installed base) and a 17% supply CAGR in the Americas.

On the power side, the U.S. Energy Information Administration forecasts electricity load growth of 1.9% in 2026 and 2.5% in 2027—the strongest four-year stretch since 2000—driven almost entirely by large computing facilities. Data centers are expected to account for roughly half of all U.S. power-demand growth through 2030. Virginia and Texas alone are already consuming 12 GW and 9.7 GW respectively. That’s not incremental growth; that’s the kind of spike that forces grid operators to tear up decade-old plans.

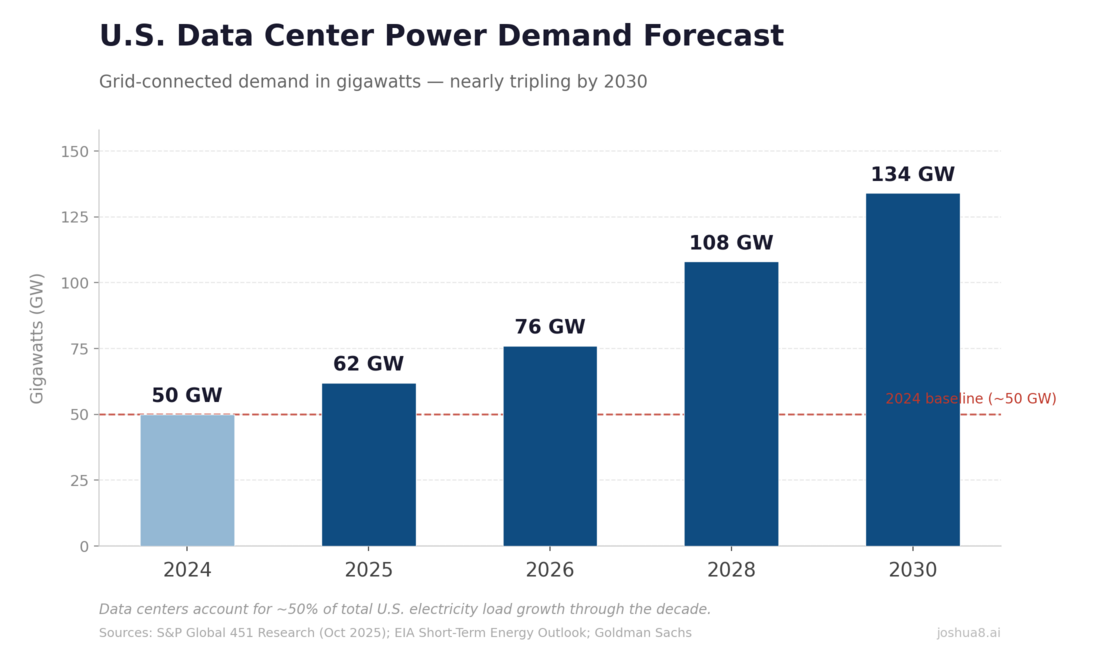

U.S. Data Center Power Demand Forecast: From ~50 GW in 2024 to ~134 GW by 2030 (S&P Global/451 Research and EIA-aligned projections). Data centers drive ~50% of total U.S. load growth through the decade.

U.S. Data Center Power Demand Forecast: From ~50 GW in 2024 to ~134 GW by 2030 (S&P Global/451 Research and EIA-aligned projections). Data centers drive ~50% of total U.S. load growth through the decade.

The Queue That Ate the Grid (and Your Timeline)

Want to feel the pain in your bones? Look at the interconnection queues.

ERCOT is sitting on more than 233 GW of large-load requests—over 70% from data centers—and the queue nearly quadrupled in a single year. That’s more demand than the entire existing Texas grid can serve today. PJM (the mid-Atlantic/Midwest operator) is processing similar volumes, with wait times stretching beyond eight years in some cases. Data centers drove 63% of the price increase in PJM’s latest capacity auction, adding $9.3 billion in costs that ultimately get passed to ratepayers.

For anyone who’s ever waited on a sewer allocation or a highway interchange approval, this is entitlements on steroids—except the “impact fees” are measured in billions and hit every business and homeowner in the region.

Lead Times: Substations Are the New Permitting Gauntlet

Here’s where it gets almost comically familiar to any CRE developer. Large power transformers still carry 120–144 week lead times (two to three years). Circuit breakers and high-voltage cable are the same. Full transmission lines? Seven to ten years.

Meanwhile, the building shell for a data center can be designed and built in 18–24 months. The substation alone now takes longer than an entire 300-unit multifamily project from permit to certificate of occupancy (Census Bureau average: 22 months for large apartment deals).

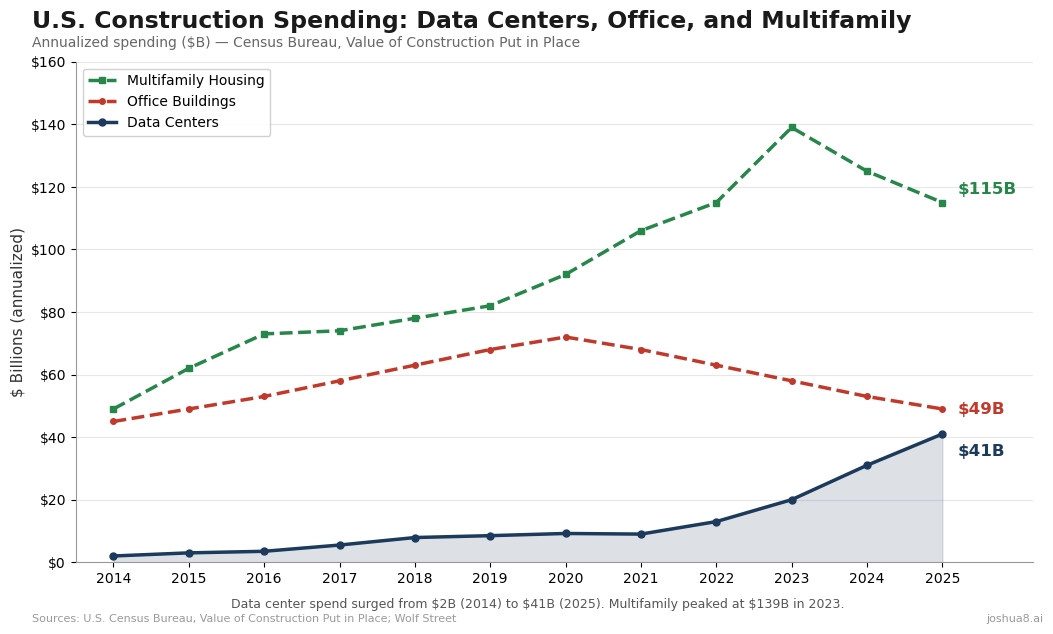

This is why “powered land” has become its own asset class—and why construction dollars are flooding here. Data center construction spending hit $41 billion in 2025 and is on track to surpass office construction by mid-2026.

U.S. Construction Spending: Data Centers, Office, and Multifamily (2014–2025). Data center spend surged from $2B to $41B annualized, up 344% since 2020, approaching office at $49B. Multifamily housing peaked at $139B in 2023 before pulling back to $115B. Source: U.S. Census Bureau.

U.S. Construction Spending: Data Centers, Office, and Multifamily (2014–2025). Data center spend surged from $2B to $41B annualized, up 344% since 2020, approaching office at $49B. Multifamily housing peaked at $139B in 2023 before pulling back to $115B. Source: U.S. Census Bureau.

Powered Land: The New Entitled Lot

Raw rural parcels that traded for $10k–$30k per acre a few years ago are now going for $200k–$1M in many markets. In Loudoun County, Virginia—the world’s densest data-center hub—industrial land is pushing above $4 million per acre, with recent infill deals exceeding $8 million according to CBRE. Salt Lake County parcels have jumped 20–40% year-over-year. The premium for sites with secured power commitments, substation proximity, or existing transmission access is routinely 2–4× what raw land commands.

Sound familiar? It’s exactly what happened when sewer capacity or highway frontage became the scarce resource in multifamily and industrial development. Developers are now securing power purchase agreements and grid allocation rights before they even option the dirt. The land follows the power—not the other way around.

Record-Low Data Center Vacancy: Primary U.S. Markets (2024–2025). Overall primary markets hit 1.4% at year-end 2025 (CBRE); Northern Virginia ~0.76%, Americas average ~4.2% (Cushman & Wakefield/JLL). Contrast with U.S. office vacancy often 15–20%+.

Record-Low Data Center Vacancy: Primary U.S. Markets (2024–2025). Overall primary markets hit 1.4% at year-end 2025 (CBRE); Northern Virginia ~0.76%, Americas average ~4.2% (Cushman & Wakefield/JLL). Contrast with U.S. office vacancy often 15–20%+.

Brownfield Repositioning: The Adaptive-Reuse Play of the Decade

The smartest players are treating this like classic CRE value-add: buy the stranded asset with the existing infrastructure. Retired power plants, old industrial sites, and facilities with grandfathered grid connections are being repositioned as data-center campuses at a fraction of greenfield cost.

Google’s $4.75 billion acquisition of Intersect Power (closed in early 2026) was fundamentally a power-and-data-center play. The $40 billion Aligned Data Centers transaction last year was the same story. Across power and utilities, M&A volume hit $141.9 billion in 2025, with a clear pivot toward dispatchable generation assets tied to data-center load.

If you’ve ever bought an obsolete warehouse for its utility connections and entitled footprint, you already know how to underwrite this.

The Full Viability Stack: Power Is First, But Not Last

Power is the headline, but the real diligence checklist looks a lot like the one you run on every multifamily or industrial deal—just scaled up and weighted differently.

Water — A 100 MW facility can pull 530,000 gallons per day for cooling. Texas data centers used roughly 25 billion gallons (direct + indirect) in 2025 and could hit 29–161 billion by 2030 in high-growth scenarios. States are already mandating closed-loop systems or reporting requirements. If you’ve fought water-rights battles in the Sun Belt, you know exactly how this story ends.

Noise & Community — The constant low-frequency hum from cooling systems is generating the same NIMBY pushback you see on multifamily projects—only louder. Setback requirements are jumping from 100 ft to 500 ft in places like Virginia. Over $162 billion in projects have faced opposition since 2023.

Labor — The national construction worker shortage sits around 439,000. Data-center projects are paying electricians and ironworkers 30%+ premiums, which means they’re directly outbidding traditional CRE jobs in the same markets. Your own multifamily or warehouse pro formas are already feeling it.

Fiber, Hazards, Soil, Transport — Dark fiber diversity, flood/seismic exposure, and the fact that a single transformer weighs 400,000 pounds (and needs special road ratings) all become make-or-break items.

The sites that clear the entire stack—power + water + noise + fiber + labor access—are exponentially more valuable than the land market suggests.

What This Means for CRE Professionals

This convergence isn’t abstract. It’s creating real opportunities and real headaches right now:

- Land banking powered sites like you used to bank entitled multifamily parcels. Power access is the new zoning approval.

- Brownfield and adaptive-reuse deals are the highest-IRR plays in the sector—exactly like repositioning Class B offices or warehouses in the 2010s.

- Diversify into data centers. With office and multifamily construction both declining from their peaks, commercial builders and GCs specializing in those segments should consider pivoting capacity toward data center projects—where spending has grown 344% since 2020 and shows no sign of slowing. The core competencies translate; the margin profiles are better.

- Labor competition is inflating costs across all CRE sectors. Factor it into your bids, or consider partnering on joint-venture sites that attract skilled trades to secondary markets.

- Water is the next power. Sites with secured water rights or closed-loop designs will command the same premium power did two years ago.

- Watch the “braggerwatt” pipeline. Announced capacity looks huge, but pre-leasing on projects under construction is 78–89%. The smart money underwrites to signed contracts and secured infrastructure—not press releases.

Bottom Line

We’ve seen infrastructure-driven value creation before—the interstate system, sewer expansions, fiber rings in the 2000s. Power is the 2026 version of that story, only bigger and moving faster than any single asset class can handle alone.

The developers and investors who treat grid interconnection queues like zoning maps, who underwrite water rights the way they underwrite parking ratios, and who spot the brownfield power-plant repositioning plays before everyone else—these are the ones who are going to make the most money in the next cycle.

Land was location. Now power is location. And the race is already on.

Navigating massive document sets for infrastructure due diligence? Contact us to see how TeraContext.AI handles the complexity at scale.