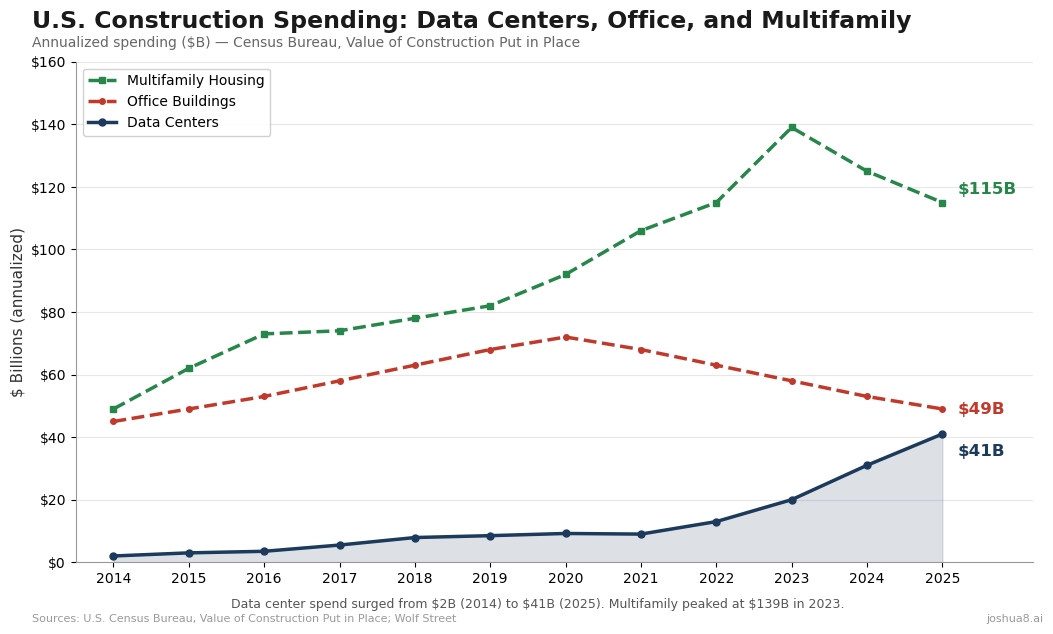

If you’re running a mid-market general contracting firm — $50 million to $500 million in revenue, built on a portfolio of commercial office towers, multifamily housing, and maybe some light industrial — you already feel the shift. Office construction spending is declining 3.6% this year and another 2% next year, and that’s with data centers propping up the overall “office” category. Strip out data centers and the core office number is in freefall. Multifamily starts have fallen sharply from their 2022 peak, dropping to roughly 380,000 units in 2025, with another 5–6% decline projected through 2027.

Meanwhile, data center construction spending hit $41 billion annualized by mid-2025 — a 25x increase from 2014 — and is on pace to surpass office construction by mid-2026. In the AGC’s latest outlook survey, 65% of contractors expect data center spending to increase in 2026, the highest net positive of any category. The global market is projected to grow from $275 billion in 2025 to $761 billion by 2034.

The revenue is migrating. The question is whether your firm migrates with it.

Data center spend surged from $2B (2014) to $41B (2025). Multifamily peaked at $139B in 2023. Office has been flat to declining for a decade. Source: U.S. Census Bureau.

Data center spend surged from $2B (2014) to $41B (2025). Multifamily peaked at $139B in 2023. Office has been flat to declining for a decade. Source: U.S. Census Bureau.

This Is Not an Office Building

The single biggest mistake a commercial GC can make is assuming that a data center is just a big box with servers in it. It is not. The entire cost structure is inverted compared to what you’re used to building.

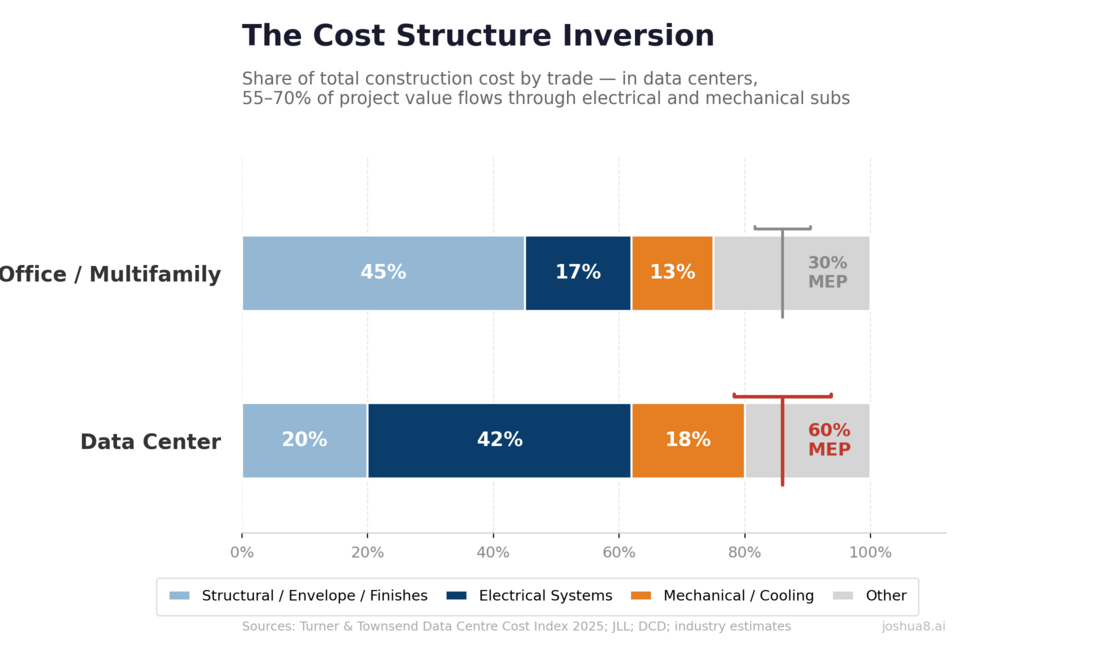

In a typical office or multifamily project, 40–50% of the construction cost is in structural, envelope, and finishes. Electrical runs 15–20%. Mechanical is 10–15%. Combined MEP is maybe 25–35% of the total.

In a data center, electrical systems alone account for 40–45% of construction cost — running $280 to $460 per gross square foot. Mechanical and cooling add another 15–20%, at $125 to $215 per square foot. Combined, 55–70% of the project value flows through electrical and mechanical subcontractors. The structural shell that’s your bread and butter? That’s down to 15–25% of the total.

The Cost Structure Inversion: In data centers, 55–70% of project value flows through electrical and mechanical subs — the inverse of traditional commercial construction. Sources: Turner & Townsend, JLL, DCD, industry estimates.

The Cost Structure Inversion: In data centers, 55–70% of project value flows through electrical and mechanical subs — the inverse of traditional commercial construction. Sources: Turner & Townsend, JLL, DCD, industry estimates.

This means your role as GC fundamentally changes. You’re no longer the builder who manages a structural and finishes job with MEP as a supporting trade. You’re a mission-critical systems integrator whose primary value is coordinating and sequencing the electrical and mechanical installation with zero tolerance for error. Overall construction costs run $600 to $1,100 per square foot — two to four times a Class A office — and the cost per megawatt of capacity is $10 to $12 million. These are $100 million to $500 million-plus projects where a single commissioning failure can cost your client millions in lost revenue per hour.

The Labor Problem: You Can’t Just Bring Your Existing Crews

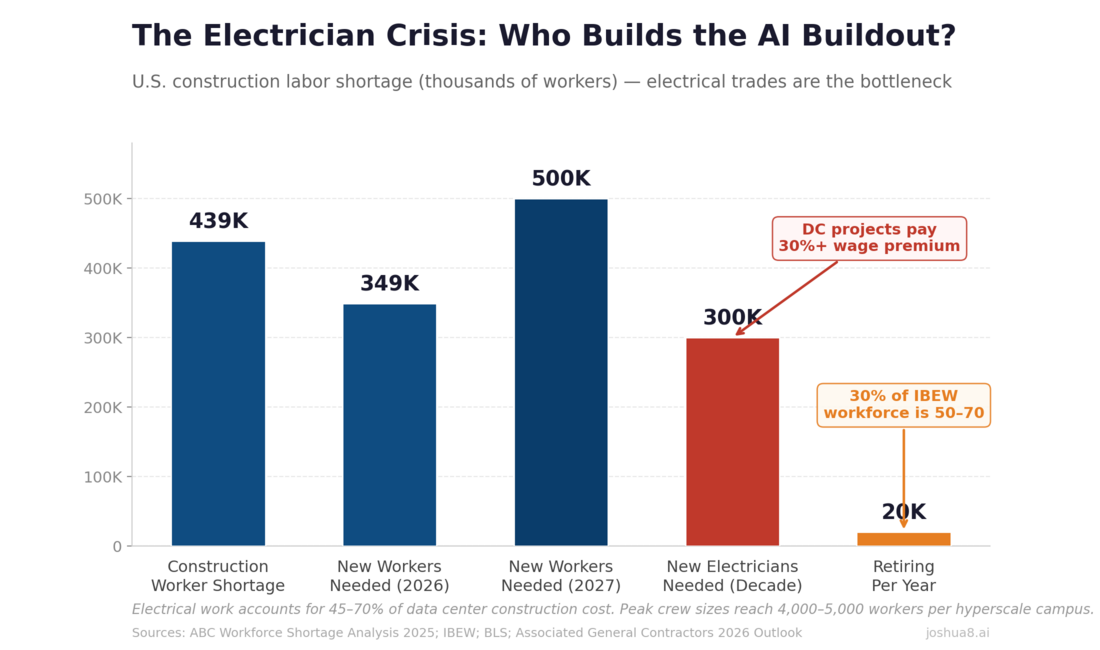

Here’s the uncomfortable truth: the trades that dominate data center construction are exactly the trades that are hardest to find in America right now.

The IBEW puts it bluntly: electrical work accounts for 45–70% of total data center construction cost, and the electrician shortage is a “life-or-death” threat to the AI infrastructure buildout. The industry needs more than 300,000 new electricians over the next decade. About 30% of the current union electrician workforce is between 50 and 70, with roughly 20,000 retiring every year. The national construction worker shortage sits at approximately 439,000, and the Associated Builders and Contractors estimates the industry needs 349,000 net new workers in 2026 alone — rising to nearly 500,000 in 2027.

439K construction worker shortage, 300K+ new electricians needed this decade, and 30% of the IBEW workforce nearing retirement. DC projects pay 30%+ wage premiums. Sources: ABC, IBEW, BLS, AGC 2026 Outlook.

439K construction worker shortage, 300K+ new electricians needed this decade, and 30% of the IBEW workforce nearing retirement. DC projects pay 30%+ wage premiums. Sources: ABC, IBEW, BLS, AGC 2026 Outlook.

The market response has been predictable: data center projects are paying 30% or more above typical construction wages. Many electrical workers on data center sites earn $100,000 to $200,000-plus. Peak crew sizes that used to top out at 750 on a large commercial project now reach 4,000 to 5,000 workers per hyperscale campus.

What does this mean for a mid-market GC trying to pivot? Three things. First, you probably can’t staff a data center project with your existing trade base — your office and multifamily electricians may not have mission-critical experience, and even if they do, the sheer volume of electrical scope will overwhelm your typical crew structure. Second, the specialty electrical subs you’ll need (Rosendin, MYR Group, Cupertino Electric, Interstates, Faith Technologies) are booked out 12–24 months and have decade-long relationships with incumbent DC builders. Third, you’re not just competing for subs — you’re competing against your own project pipeline, because those same electricians are the ones your multifamily and office projects need too.

Where Do You Get the Design Expertise?

Data center design is a specialized discipline that your current AE relationships probably don’t cover. The building’s structural design might be straightforward, but the MEP design — power distribution, redundancy pathways, cooling architecture, fire suppression, monitoring systems — requires engineers who understand concurrent maintainability, fault tolerance, and Uptime Institute tier classification at a system-by-system level.

The good news: there’s a well-established ecosystem of DC-specialized design firms actively looking for new construction partners as the market expands beyond what incumbent builders can serve. On the architecture side, Corgan (the #1 ranked DC architecture firm), HDR, Gensler, Stantec, and AECOM lead the field. On the engineering side, Burns & McDonnell (#1 DC engineering firm), Jacobs, and WSP dominate, with strong regional players like Woolpert, Kimley-Horn, and Olsson filling the mid-market.

The most direct path for a mid-market GC is a design-build teaming arrangement: you partner with a DC-experienced AE firm as the design lead while your firm provides construction management, local trade relationships, and the boots-on-the-ground execution. This gives you the design credibility you lack while leveraging the capabilities you already have — procurement, scheduling, safety management, concrete and steel execution, and local jurisdiction knowledge.

The other critical hire is a data center program director — an experienced construction executive recruited from an incumbent firm like DPR, Holder, Hensel Phelps, or Turner who brings the rolodex, the technical knowledge, and the owner relationships your firm needs to be credible in the prequalification process. This is probably the single highest-ROI investment a pivoting GC can make.

The Prequalification Catch-22 (and How to Break It)

Every data center owner and operator has the same prequalification checklist: documented completed DC projects with MW capacity and tier level, owner references from mission-critical facilities, EMR under 1.0, OSHA 30-hour certified supervisors, strong bonding capacity ($5M+ GL insurance), and demonstrated commissioning experience.

The obvious problem: you need data center experience to win data center work, and you can’t get data center experience without data center work. This is the same Catch-22 that every GC has faced when entering a new sector, and the solutions are the same — you break in from the edges and work toward the center.

Start with powered shell and white box. Many hyperscalers separate their projects into shell/core and fit-out contracts. The shell — concrete, steel, building envelope, site work — is essentially what you already build. You don’t need mission-critical MEP experience to pour a foundation and erect a tilt-up shell designed to data center specs. This gets you on the owner’s radar, on the site, and in the reference database.

Bid adjacent infrastructure. Every data center campus needs substations, utility corridors, access roads, parking, fencing, security buildings, and sometimes water treatment facilities. These are standard GC scope items that happen to be on a data center site. They build your resume in the ecosystem without requiring you to touch mission-critical systems.

Joint venture with an experienced partner. Team with an established DC builder where you handle civil and structural scope while they handle mission-critical MEP. You both get what you need: they get local labor and jurisdiction knowledge; you get DC experience and an owner reference. After two or three successful JVs, you can start bidding independently.

Target colocation and edge facilities. Hyperscale data centers (50–500+ MW) are the hardest entry point — the owners are sophisticated, the stakes are enormous, and the incumbent builders have locked-in relationships. Colocation facilities (5–20 MW) have more accessible owners, lower risk tolerance thresholds, and more project volume spread across more sites. Edge data centers are even smaller and often built by the same types of firms that build commercial offices.

How to Build Your Subcontractor Network

The specialty sub question is the hardest part of the pivot, and there’s no shortcut. But there are strategies.

Recruit from within the trades. IBEW locals in your market are training new apprentices, and some journeymen electricians are looking for opportunities with firms that will invest in their data center career path. If you can offer a DC training pipeline — paid Uptime Institute certifications, manufacturer training, mentorship under experienced mission-critical electricians — you become an employer of choice for ambitious tradespeople.

Partner with Tier 2/3 electrical subs who want to scale. Not every project needs Rosendin. There are regional electrical contractors with strong commercial capabilities who are eager to move into mission-critical work but lack the GC relationships to win it. You grow together — they bring the electrical execution capacity, you bring the project access and management infrastructure. This is how new supply chains form.

Invest in prefabrication. Power skids, cooling assemblies, electrical rooms, and integrated rack systems are increasingly assembled and tested off-site, with highly modularized projects achieving 30–50% schedule reduction. If your firm develops or acquires prefab capabilities — off-site fabrication yards, advanced BIM coordination, logistics management — you can compete on schedule, which is the metric hyperscalers care about most. Prefab also reduces the on-site labor requirement, partially offsetting the electrician shortage.

Lock in long-term relationships early. Rosendin reportedly has customers providing work forecasts 10–20 years out. The successful DC subs are thinking in decades, not projects. If you can offer a multi-project pipeline to a specialty sub — even if the first project is small — you become a more attractive partner than a one-off bid.

The Certifications That Matter

Send your key people to training now, before you need it on a bid:

Uptime Institute Accredited Tier Designer (ATD) and Accredited Tier Specialist (ATS) are the gold standard that owners look for. BICSI’s Data Center Design Consultant (DCDC) certification covers telecommunications infrastructure. ASHRAE certifications matter for your mechanical team. And NFPA 70E (electrical safety) is already standard in commercial work but is absolutely non-negotiable in data centers.

The investment is modest — typically $2,000–$5,000 per certification per person — but having two or three ATD/ATS-certified staff members on your prequalification submittal immediately signals credibility that no amount of marketing can replicate.

The Risk You Need to Manage

Some contractors in the AGC survey flagged a legitimate concern: over-dependence on a single sector. If AI investment cools — if the “braggerwatt” pipeline collapses and data center demand softens in 2027 or 2028 — firms that went all-in on DC could face a painful correction. The smart play is to pivot part of your capacity, not all of it. Maintain your multifamily and light industrial relationships. Diversify within the data center space across hyperscale, colocation, and edge segments. And underwrite your DC pipeline to signed contracts, not press releases.

The other risk is cultural. Data center owners operate in a world of 99.999% uptime, where minutes of downtime cost millions. A missed handover date or a quality issue that would be a punch-list item on a multifamily project can be a career-ending failure in mission-critical construction. The commissioning process alone — Integrated Systems Testing where every breaker, transfer switch, and chiller is tested under simulated load and failure conditions — is more rigorous than anything in commercial construction. Invest in commissioning expertise before you bid, not after.

The 18-Month Playbook

If you’re a mid-market GC watching your office and multifamily pipelines shrink while data center spending rockets past $41 billion, here’s the action plan:

Months 1–3: Foundation. Hire a DC program director from an incumbent firm. Send 3–5 key people to Uptime Institute and BICSI certification courses. Identify 2–3 DC-specialized AE firms for design-build teaming. Map the specialty electrical and mechanical subcontractor landscape in your market.

Months 4–9: Entry. Bid powered shell, adjacent infrastructure, and colocation/edge projects. Form at least one JV with an experienced DC builder. Establish relationships with regional electrical subs who want to grow into mission-critical work. Invest in prefab/modular capabilities.

Months 10–18: Scale. Complete your first DC project (even if it’s just a shell). Use that reference to pursue larger scopes. Deepen sub relationships into multi-project commitments. Begin pursuing full-scope DC projects with your design-build AE partner.

The firms that make this pivot successfully won’t abandon their commercial roots — they’ll use them as an entry ramp. The concrete, steel, scheduling discipline, and safety culture you’ve built over decades are real assets in data center construction. What you’re adding is a layer of mission-critical expertise, a new subcontractor network, and an entirely different relationship with electrical and mechanical systems.

The revenue is moving. The subs are moving. The design firms are looking for new partners. The question isn’t whether mid-market GCs can crack the data center market — it’s which ones will move first.

A Note on What’s Coming Next: AI-Dense Facilities

The cost breakdowns in this post are based on conventional and colocation data center averages — the numbers that published cost indices from Turner & Townsend and JLL still report on. But the newest AI training facilities are a different animal entirely.

Conventional colocation runs 5–15 kW per rack. AI training clusters with NVIDIA GB200 NVL72 configurations are pushing 120–140 kW per rack — a 10x density increase that reshapes the cost structure even further. Electrical’s share climbs higher as power distribution, busway, switchgear, and UPS systems scale with density — more power per square foot means more copper, more transformers, more redundancy in a smaller footprint. Cooling costs surge because air cooling simply can’t handle these densities; AI facilities are moving to direct-to-chip liquid cooling, rear-door heat exchangers, and immersion cooling, pushing the mechanical line item from 18–20% to 22–28% of total cost. Meanwhile, structural’s share shrinks further — simpler envelopes (no raised floors in many modern designs), but significantly higher floor loading requirements for liquid cooling infrastructure and denser rack configurations.

The bottom line: for an AI-optimized facility, MEP’s share is probably closer to 70–75%, not 60%. The cost structure inversion gets even more dramatic — and the need for electrical and mechanical expertise becomes even more acute.

That’s the subject of our next post. Stay tuned.

Managing massive document sets for data center construction due diligence? Contact us to see how TeraContext.AI handles specs, RFIs, and compliance at scale.