You can build the building in 18 months. Getting power to it takes seven years. The firms solving that equation are building their own power plants — and the GCs who can deliver that scope will own the next cycle.

TL;DR for Transitioning GCs

If you’ve been following this series, you know the data center market is splitting between conventional and AI-dense facilities. But here’s what nobody told you: the hardest part of building an AI data center isn’t the liquid cooling, the structural loading, or the 800-volt DC power. It’s getting enough electricity to the site in the first place.

The grid can’t keep up. Interconnection queues run 3–7 years in most U.S. markets. Google was told by one utility it would take 12 years just to evaluate a connection request. Developers are looking to add 16 GW by 2026, but only 5 GW has started construction. Roughly half of planned 2026 AI capacity is at risk of delay — and the bottleneck is power, not permits or materials.

Operators are building their own power plants. OpenAI and Oracle ordered 2.3 GW of on-site gas generation for the Stargate project in Texas. xAI deployed over 900 MW of gas turbines across two Memphis-area sites. Bloom Energy can deliver 100 MW of fuel cells in 120 days — faster than most utilities can process an application. More than a third of U.S. gas power capacity under development is earmarked for behind-the-meter data center use.

Transformers and switchgear are the new bottleneck. Large power transformer lead times average 128 weeks. Demand for generator step-up transformers is up 274% since 2019. A single hyperscale campus needs dozens of transformers weighing 100,000+ pounds each. If you don’t lock in procurement 2–3 years out, you don’t have a project.

Your electrical scope doubles. The traditional data center electrical chain — utility feed, transformer, UPS, PDU, rack — is being replaced by a two-tier system. Tier 1 is power plant and substation work: 138kV interconnection, customer-owned substations, gas turbine pads, fuel cell yards, and battery storage. Tier 2 is facility distribution: medium-voltage switchgear, 800 VDC rectifiers, busbars. GCs who can deliver both tiers — or at least coordinate them — will command the premium projects.

The money is real. PJM capacity prices jumped 833% in one year. On-site generation avoids that escalation. Power infrastructure now represents 30–40% of total AI data center project cost. The firms that figure out power delivery will build the biggest projects of the next decade.

Read on for the details.

The Seven-Year Wait

Every data center project starts with the same question: where does the power come from?

For conventional facilities, the answer was straightforward. Call the utility, request a service upgrade, negotiate an interconnection agreement, build a substation, and you’re online. The process took 12–18 months in most markets and was well within the competence of any experienced electrical contractor.

That world is gone.

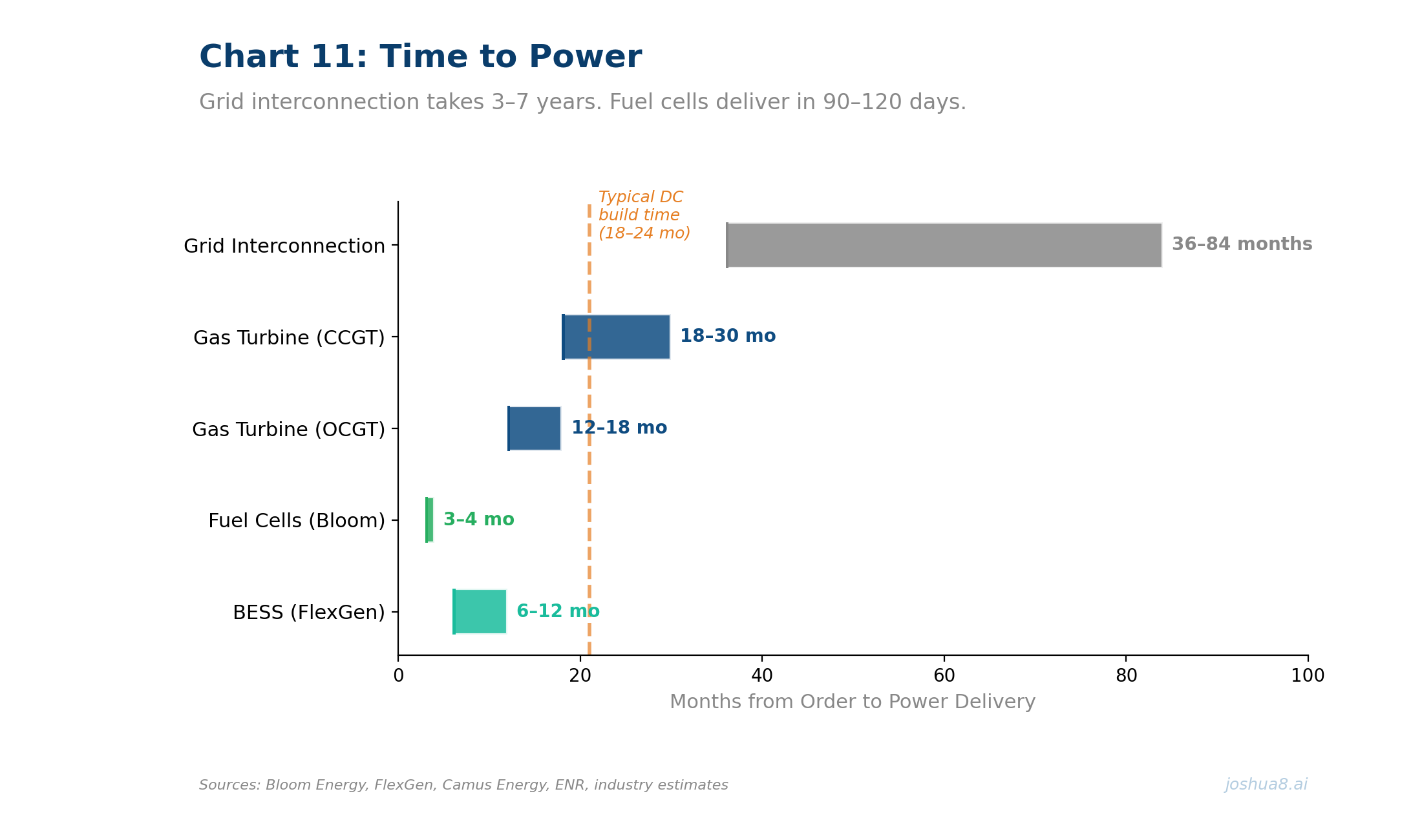

Grid interconnection timelines across the United States have stretched to 3–7 years in most markets. In congested territories like PJM — the regional grid operator covering 13 states and the District of Columbia — the queue is so backed up that developers face multi-year waits just to get a study completed, let alone construction authorization. Google’s global head of sustainability has publicly stated that utilities “often require four to ten years to connect new loads.” In one case, a utility told Google it would need 12 years to evaluate a single interconnection request.

The numbers tell the story. Developers are trying to add at least 16 gigawatts of new data center capacity by 2026. Construction has started on roughly 5 gigawatts. That leaves 30–50% of planned 2026 AI capacity at risk of delay, and in most cases the constraint isn’t construction labor, materials, or even permitting — it’s power availability. New data center capacity additions fell 50% quarter-over-quarter in Q4 2025, not because demand softened but because power queues hardened.

Engineering News-Record put it plainly: “Grid access, not land, emerges as bottleneck for data center construction.”

For GCs transitioning from office and multifamily, this is critical context. The projects that actually get built are the ones that solve the power problem. If you’re bidding a data center job and nobody has addressed power delivery, you’re bidding a project that may not happen.

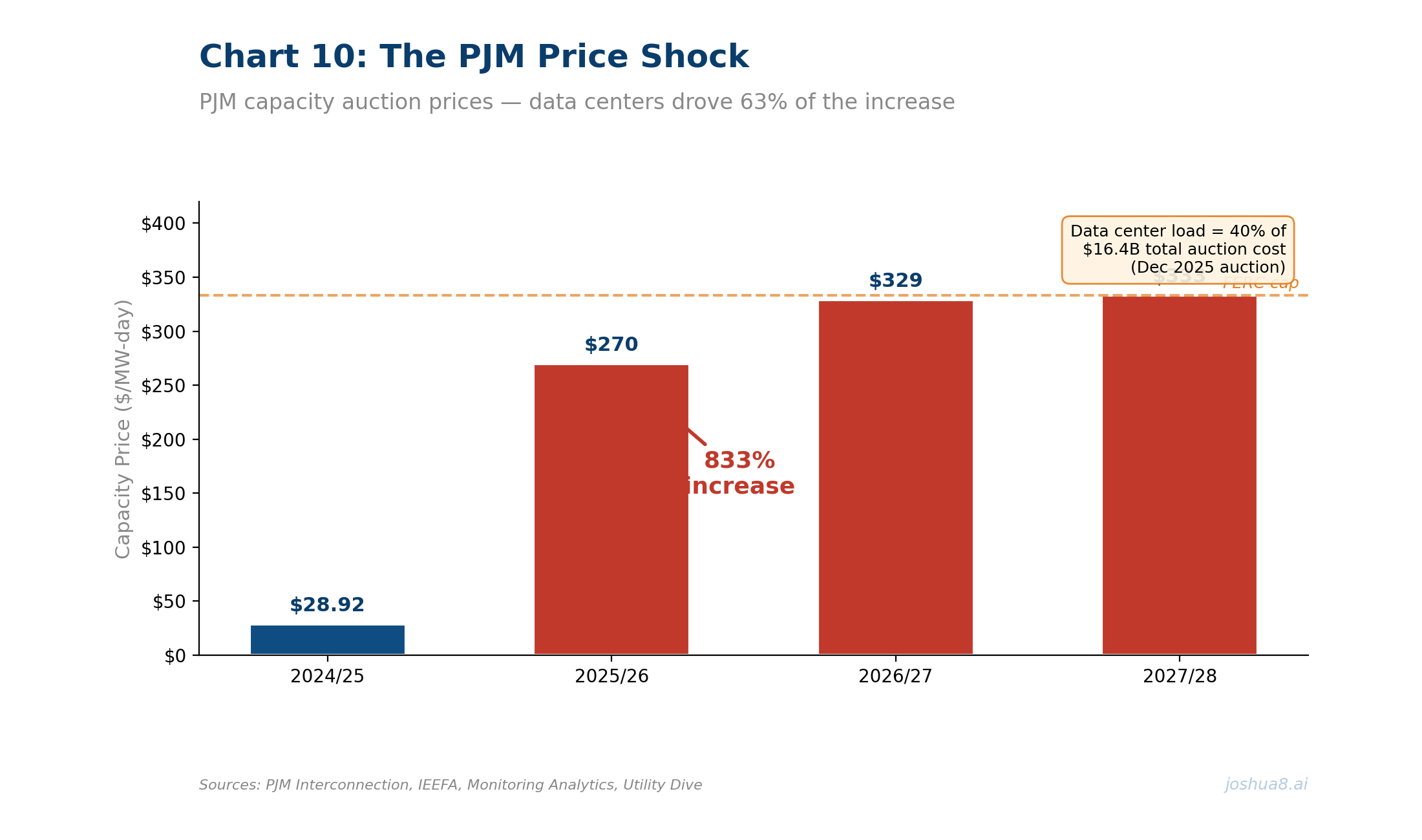

The Price Shock: 833% in One Year

Even when grid power is available, the cost of securing it has exploded.

PJM runs competitive capacity auctions where generators bid to provide power reliability. These auctions set the baseline cost of electricity for 65 million people across the mid-Atlantic and Midwest. The trajectory over the past three years tells you everything about where this market is heading:

| Delivery Year | Capacity Price ($/MW-day) |

|---|---|

| 2024/2025 | $28.92 |

| 2025/2026 | $269.92 |

| 2026/2027 | $329.17 (FERC cap) |

| 2027/2028 | $333.44 (FERC cap) |

That’s a 10× increase from 2024 to 2027. PJM’s independent market monitor, Monitoring Analytics, estimated that data centers were responsible for 63% of the price increase in the 2025/2026 auction — translating to $9.3 billion in additional costs recovered from all ratepayers. In the December 2025 auction, data center load accounted for $6.5 billion, or 40%, of the total $16.4 billion cost.

PJM projects that peak demand will grow by 32 gigawatts between 2024 and 2030. All but 2 gigawatts of that growth is expected to come from data centers.

The downstream effects are already hitting consumers. Washington D.C. Pepco customers saw bills increase roughly $21 per month starting in June 2025. New Jersey experienced a 21.6% increase. These are the political costs of data center growth, and they’re accelerating the push toward behind-the-meter generation — if operators make their own power, they don’t drive up the rates for everyone else.

For GCs, the takeaway is this: the economics of on-site power generation improve every time the grid gets more expensive. And the grid is getting more expensive fast.

The Transformer Crisis

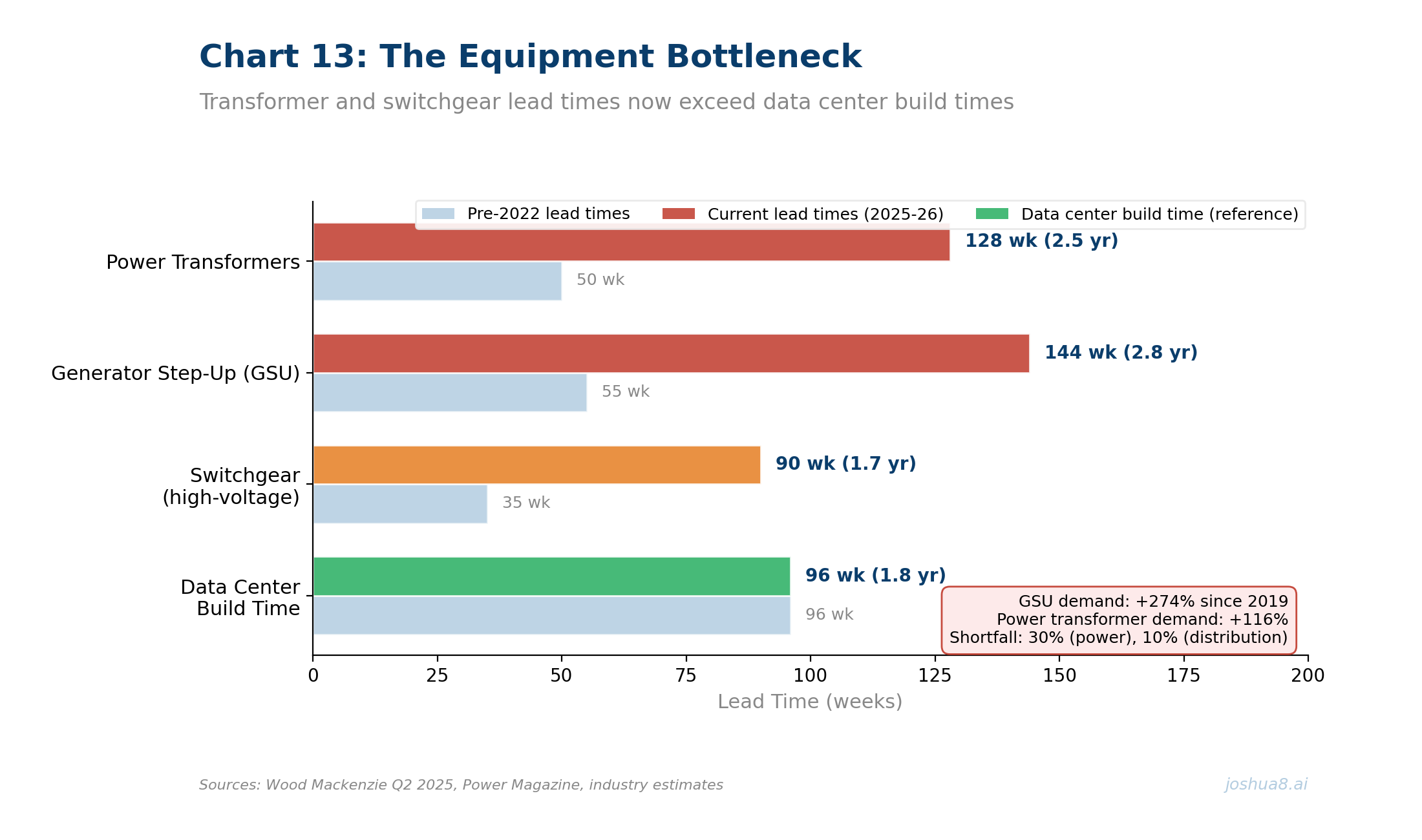

Even if you solve the interconnection queue and the capacity pricing, you still have to physically build the electrical infrastructure. And the equipment you need has a multi-year lead time.

Large power transformers — the kind required for a hyperscale data center substation — now average 128 weeks from order to delivery. Generator step-up units average 144 weeks. Switchgear lead times have climbed from sub-35 weeks to over 44 weeks. Since 2019, demand for generator step-up transformers has grown 274%. Substation power transformers are up 116%.

Wood Mackenzie estimates a 30% shortfall for power transformers and 10% for distribution units across the national fleet in 2025. A single hyperscale campus requires dozens of large power transformers, each weighing 100,000 pounds or more. The competition for these units is intense, and it’s not just data centers — utilities, renewable energy projects, EV charging infrastructure, and industrial reshoring are all chasing the same constrained supply.

The manufacturing base is responding, but slowly. Hitachi Energy is investing over $1 billion including a $457 million facility in South Boston, Virginia. Siemens Energy is building a $150 million plant in Charlotte, North Carolina, with production expected in early 2027. Eaton has committed $340 million to a facility in South Carolina, also targeting 2027. But even with these investments, meaningful relief in lead times isn’t expected before 2027–2028.

What this means for construction: transformer and switchgear procurement must now happen at the front of preconstruction — 2 to 3 years before the facility is scheduled to go live. This is a fundamental shift in project sequencing. In commercial construction, major equipment procurement typically happens during the construction phase. In data center construction, it happens before design development is complete. GCs who don’t understand this sequencing will lose projects to firms that do.

Building Your Own Power Plant

When the grid can’t deliver power on your timeline, at your price, you build your own. This is the defining trend in AI data center construction: the shift from utility-dependent facilities to behind-the-meter (BTM) generation, where the data center operates its own power plant on-site.

The scale is staggering. More than one-third of all U.S. gas-fired power capacity currently under development is slated to directly power data centers behind the meter. Bloom Energy’s 2026 Power Report projects that one-third of data centers will be fully off-grid by 2030. Ireland and Texas have begun implementing “bring your own power” mandates for large-load customers.

The economics are straightforward: if PJM capacity prices are running $329/MW-day and climbing, and you can build your own combined-cycle gas plant for roughly $2 million per MW of capacity, the payback period for on-site generation is shrinking every year. Add the 3–7 year interconnection delay you avoid, and behind-the-meter generation isn’t just cheaper — it’s the only way to build on any reasonable timeline.

This has massive implications for GCs. You’re no longer building a data center. You’re building a data center and a power plant on the same site, on the same schedule, often with the same owner. The firms that can deliver both scopes — or at minimum, coordinate both scopes under a single project management structure — are the ones winning the largest projects.

The Gas Turbine Boom

Natural gas turbines are the dominant technology for large-scale behind-the-meter data center power today. The order books tell the story.

Siemens Energy nearly doubled its global gas turbine sales from 100 units in 2024 to 194 units in 2025 — record volume driven overwhelmingly by data center demand. GE Vernova saw new gas turbine orders nearly triple year-over-year, reaching 55 gigawatts. Siemens is investing $1 billion in U.S. manufacturing expansion to keep up.

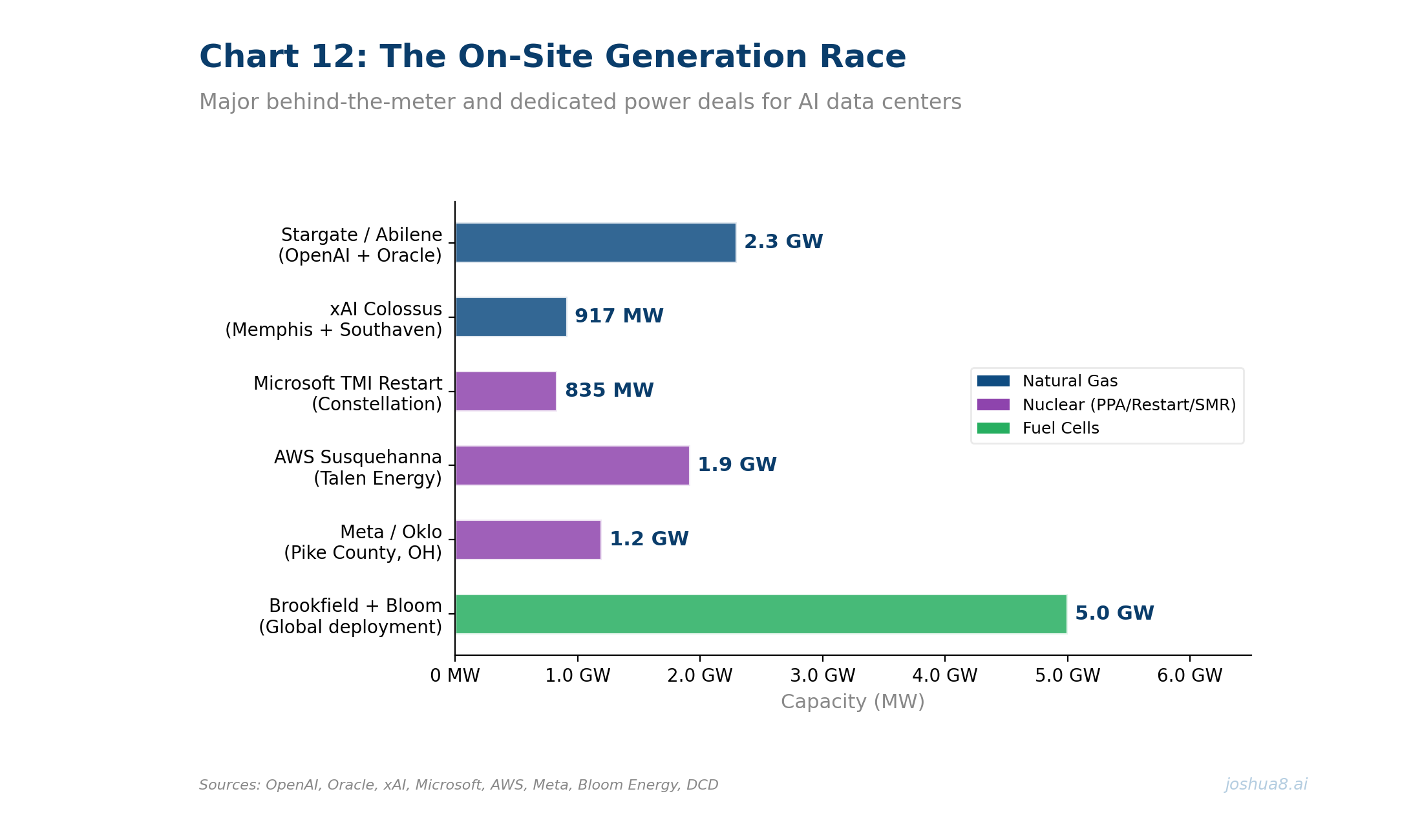

Two projects illustrate the scale of what’s happening.

Stargate / Abilene, Texas: OpenAI and Oracle’s Stargate initiative signed a deal with VoltaGrid for 2.3 gigawatts of natural gas microgrid capacity — the largest on-site generation order in data center history. The Abilene campus alone spans 4 million square feet with 1.2 GW of total power capacity, expected to complete in mid-2026. A second site in Shackelford County received Texas Commission on Environmental Quality approval for 210 industrial gas generators with 700 MW of combined capacity — 197 engines for primary power, 13 for backup. Parker Hannifin is supplying turbine equipment for over 1 GW at Abilene. This is not a backup generator farm. This is a power plant that happens to have a data center next to it.

xAI Colossus / Memphis, Tennessee: Elon Musk’s xAI deployed 35 gas turbines generating 422 MW at its Colossus supercomputer facility, plus an additional 27 turbines generating 495 MW at a second site in Southaven, Mississippi. Total on-site gas generation across the two locations: roughly 917 MW — comparable to a mid-sized utility power station. The facility also draws 150 MW from the local utility. The project became a cautionary tale in permitting: xAI operated many of these turbines without appropriate air quality permits, triggering community opposition and environmental enforcement actions. The Southern Environmental Law Center called it “an illegal power plant.”

Capital costs for gas turbines: Combined-cycle gas turbine plants (higher efficiency, larger footprint) run approximately $1.6–2.5 million per megawatt installed. Simple-cycle turbines (faster to deploy, lower efficiency) run approximately $0.7–1.3 million per megawatt depending on configuration and scale. At scale, combined-cycle costs can drop below $700/kW. Gas turbines deliver approximately 50 MW per acre of land.

The construction scope for a gas turbine installation includes foundations (reinforced concrete pads rated for vibration and thermal cycling), fuel gas supply piping, exhaust stacks, electrical interconnection to the facility’s medium-voltage bus, cooling systems (if combined cycle), control building, fire suppression, and emissions monitoring equipment. This is industrial power plant construction — it requires mechanical contractors with power generation experience, not commercial HVAC firms.

Fuel Cells: The Speed Play

If gas turbines are the volume play, fuel cells are the speed play. And in a market where time-to-power determines whether your project happens at all, speed matters enormously.

Bloom Energy, the market leader in solid oxide fuel cells for data centers, can deliver 50 MW of capacity in as little as 90 days and 100 MW in 120 days — assuming gas supply and permits are in place. Compare that to 12–18 months for gas turbine procurement and installation, or 3–7 years for grid interconnection. In a market where every month of delay costs tens of millions in lost revenue, the ability to deploy 100 MW in four months is a transformative advantage.

Bloom has already deployed over 400 MW to data centers worldwide, with 1.5 GW across 1,200+ installations globally. The company is scaling production capacity to 2 GW per year by end of 2026. Partnerships with AEP, Equinix, and Oracle are active.

The marquee deal: Brookfield signed a $5 billion strategic partnership with Bloom Energy to deploy fuel cell technology at AI data centers globally. This is the largest single investment in fuel cell infrastructure in history.

Why fuel cells for data centers?

Fuel cells deliver up to 100 MW per acre — double the density of gas turbines. For constrained urban or suburban sites, this is decisive. They run 10–30% more efficiently than gas turbines because the electrochemical reaction that generates electricity doesn’t involve combustion, reducing both fuel consumption and emissions per megawatt-hour. Capital costs run 10–15% higher than gas turbines on a nameplate basis, but the gap narrows when you factor in the redundancy overbuild required for gas turbine microgrids to achieve utility-grade availability.

For GCs, the construction scope for fuel cell installations is more modular than gas turbines: concrete pads, gas supply piping, electrical interconnection, and Balance of Plant (BoP) equipment. Bloom’s fuel cell units are factory-assembled and shipped as modules, which means the on-site construction is primarily site preparation, utilities, and interconnection rather than heavy mechanical assembly. This is closer to equipment installation than power plant construction — a different skill set from gas turbines, and potentially more accessible for GCs entering the market.

BESS: The Diesel Killer

The traditional data center backup power model — rows of diesel generators on concrete pads behind the building — is being replaced by battery energy storage systems (BESS) that do everything diesel can do and more.

In June 2025, FlexGen and Rosendin launched the BESSUPS — the first utility-scale battery system designed as a full UPS replacement for data centers. The system sits outside the data center building, connecting at medium voltage (1,000V to 35,000V), which eliminates traditional UPS infrastructure inside the facility. This simplifies the building’s internal electrical architecture, reduces indoor equipment footprint, and cuts capital expenditure on conventional UPS hardware.

The BESSUPS integrates FlexGen’s HybridOS energy management system with patented technologies for soft grid interconnection and island-mode frequency stabilization. The companies are performing real-world, grid-connected tests proving that utility-scale BESS can meet the waveform control requirements of mission-critical data center loads.

Why BESS beats diesel:

Traditional UPS systems provide seconds to minutes of bridge power — enough time for the diesel generators to start and synchronize. BESS provides 4–8 hours of extended backup, which in many scenarios eliminates the need for generators entirely. BESS is bidirectional: it can export power to the grid during peak demand, creating a revenue stream that offsets the capital cost. No diesel fuel logistics, no underground storage tanks, no periodic load-bank testing, no emissions. And no community opposition to diesel exhaust — an increasingly potent permitting barrier.

Microsoft deployed Saft battery systems at its Stackbo, Sweden facility — four 4 MWh units providing both backup power and grid services. This dual-use model is becoming the standard: the batteries earn revenue when they’re not needed for backup.

For GCs, BESS construction scope includes reinforced concrete pads (rated for the weight of battery containers, typically 40,000–60,000 lbs per unit), medium-voltage switchgear, grid interconnection equipment, fire suppression systems (NFPA 855 compliance), thermal management, and fencing/security. The pad and electrical work are well within the capability of commercial electrical contractors, but the system integration and commissioning require specialized expertise from the BESS vendor and their certified integrators.

800 VDC: The Electrical Revolution Inside the Building

While the generation and delivery of power are transforming outside the building, the distribution of power inside the building is undergoing its own revolution.

NVIDIA’s reference architecture for Vera Rubin-era AI factories transitions from the traditional 415V AC distribution to 800V DC. The conversion happens at the building perimeter: industrial-grade rectifiers take 13.8 kV AC from the grid (or on-site generation) and convert it directly to 800 VDC, which is then distributed through busbars to the racks.

The benefits are significant. An 800 VDC system can transmit 85% more power through the same conductor size compared to AC. Copper requirements drop by 45% versus traditional low-voltage DC systems. In a 1 GW data center, that’s the difference between 200,000 kg of copper busbars and roughly 110,000 kg — a material cost savings in the tens of millions. The simplified architecture — fewer transformers, no phase-balancing equipment, fewer conversion stages — also means fewer points of failure and higher reliability.

NVIDIA’s 800 VDC rollout is targeted for 2027, with ecosystem partners including ABB, Eaton, Texas Instruments, Infineon, and a dozen other silicon and power infrastructure companies. TI unveiled a complete 800 VDC power architecture for AI data centers with NVIDIA in March 2026.

What this means for electrical contractors:

This is not incremental change. Most commercial electricians have spent their careers working with 120/208V or 277/480V AC systems. The jump to 800 VDC requires fundamentally different skills:

Medium-voltage work (13.8kV or 34.5kV) inside the building requires electricians with 15kV switchgear experience — this is industrial power distribution, not commercial. DC arc flash hazards behave differently than AC — different clearing times, different PPE requirements, different NFPA 70E procedures. Busbar installation replaces traditional cable tray and conduit runs. Rectifier rooms replace traditional UPS and PDU rooms. The testing and commissioning protocols for DC distribution are distinct from AC.

The firms that retrain their workforce for 800 VDC and medium-voltage DC distribution will own the electrical scope on the highest-value data center projects for the next decade. Everyone else will be left competing for conventional AC facilities — a shrinking share of the market.

Nuclear: The Horizon Play

Every major hyperscaler is investing in nuclear power for data centers, but the timelines are long and the construction implications are a generation away.

Microsoft’s 20-year power purchase agreement with Constellation Energy to restart the 835 MW Three Mile Island Unit 1 reactor targets 2028 — Constellation is investing $1.6 billion in the restart, with an estimated $16 billion GDP impact to Pennsylvania. Amazon’s $20 billion investment around the Susquehanna nuclear plant in Pennsylvania includes a 17-year, 1.92 GW power purchase agreement through 2042. Google signed the first U.S. corporate SMR fleet deal with Kairos Power for 500 MW, targeting 2030+. Meta partnered with Oklo to develop a 1.2 GW campus in Ohio with 16 Aurora Powerhouse reactors, first units expected around 2030. Amazon is also planning 12 small modular reactors in Washington state.

These are multi-billion-dollar commitments that signal where the industry is headed. But no U.S. data center is currently powered by an SMR, and the most optimistic first-commercial-operation dates are 2030–2032. NuScale’s design is NRC-certified. Oklo and Kairos are pursuing licensing. The regulatory, environmental, and construction certification requirements for nuclear are an entirely different industry from commercial or even industrial construction.

For GCs: nuclear is worth watching but not worth staffing for today. When SMR-powered data center campuses arrive, they’ll require nuclear-grade civil construction (NQA-1 quality programs), separate licensing, and specialized security infrastructure. The GCs who build them will be firms with nuclear construction experience, or joint ventures between data center builders and nuclear constructors. That’s a 2030s story.

What This Means for Your Next Bid

Lead with power. Before you bid structural, mechanical, or architectural scope, ask the fundamental question: where does the power come from and when? If the answer involves a utility interconnection queue, understand the timeline and who owns the risk. If the project includes behind-the-meter generation, make sure your bid accounts for the power plant scope or clearly defines the interface.

Procure transformers and switchgear immediately. At 128–144 week lead times, electrical equipment procurement must happen at the very beginning of preconstruction — potentially before schematic design is complete. GCs who make this their first call on a new project will deliver on schedule. GCs who wait until construction documents are issued will wait two more years.

Build power plant relationships. The firms building on-site generation — VoltaGrid, Enchanted Rock, Bloom Energy, and the EPC contractors who install Siemens and GE Vernova turbines — are becoming essential partners for data center GCs. If your subcontractor list doesn’t include a power generation EPC firm, you can’t bid the largest projects.

Understand fuel cells as a fast-track option. When a project needs power in months rather than years, fuel cells are the answer. Bloom can deploy 100 MW in 120 days. For GCs, the site preparation scope — pads, utilities, interconnection — is relatively straightforward and can differentiate your proposal on schedule.

Budget for BESS instead of diesel. The BESSUPS model — utility-scale battery replacing traditional diesel generators and indoor UPS — is the direction of the industry. Factor BESS pad construction, medium-voltage interconnection, and NFPA 855 fire suppression into your site work scope.

Retrain your electricians for 800 VDC. NVIDIA’s rollout targets 2027. The projects being designed today for 2028 occupancy will specify 800 VDC distribution. Electricians who understand DC power systems, medium-voltage switchgear, and busbar installation will command premium rates. Start the training pipeline now.

The Bottom Line

The AI data center isn’t just a building that consumes power. It’s a power project that happens to contain a building.

The grid can’t deliver power fast enough. Utilities can’t build substations fast enough. Transformer manufacturers can’t produce equipment fast enough. So the industry is doing what it always does when infrastructure can’t keep up with demand: building its own.

For GCs coming from commercial construction, this is the final piece of the puzzle. Blog 1 in this series showed you the demand. Blog 2 showed you how to pivot. Blog 3 showed you what the buildings look like. This post shows you what makes them run: on-site gas turbines and fuel cells generating hundreds of megawatts, battery systems replacing diesel generators, customer-owned substations connecting at transmission voltage, and 800-volt DC distribution eliminating the AC infrastructure you’ve spent your career installing.

The total U.S. investment in grid and power infrastructure driven by data center demand — generation, transmission, distribution, and storage — is projected to run into the hundreds of billions of dollars through 2030. The firms that master this scope won’t just build data centers. They’ll build the power plants that make data centers possible.

That’s the opportunity. It’s not a building contract. It’s a power contract that includes a building.

This is part of an ongoing series exploring where traditional construction and digital infrastructure collide. Previous posts: Power Is the New Land, The Builder’s Pivot, and Building for the Next GPU.